New York City is making national headlines once again, as charismatic new Mayor Zohran Mamdani puts forth plenty of controversial new proposals as he takes the helm of America's largest city. Should holders of NYC municipal bonds be concerned, or is it a tempest in a teapot? Read on for our current thinking.

Although disco and bellbottom jeans fell out of favor after the 1970s, not everything from that decade faded with the times. New York City's modern fiscal foundation is built upon the practical lessons learned from its brutal 1975 financial crisis. Understanding the situation in place today requires some knowledge of the far-reaching consequences of that game-changing emergency.

Without getting too far into the weeds, in the mid-70s NYC suddenly found itself in a serious budgetary bind. After many years of gross budgetary mismanagement, amplified by the knock-on effects from a persistent nationwide economic recession, City officials ran out of room to kick the can down the road any further. Cash was in short supply and a money default on its bonds was a near certainty absent a bailout from the federal or New York State government.

After some very public drama, a bailout was ultimately organized and default was avoided. But the end of that story is where our interest begins. The upshot is that the bailout came with terms that forced key changes to the way the City planned and operated, with the objective of preventing similar crises from developing in the future.

Most of those favorable changes are still in place today:

Pre-crisis, even high-ranking NYC officials and civil servants demonstrated a near-total lack of understanding of its true financial situation - there are legendary stories of how the City couldn’t even keep track of its own cash! Since then, this dynamic has completely flipped: NYC municipal government is now widely considered a paragon of strong financial controls, and is the only major American city that budgets and plans using Generally Accepted Accounting Principles (GAAP), the gold standard for reality-based financial analysis.

Forward-planning, once a complete afterthought, is now also a notable strength. NYC consistently puts out detailed multi-year operating and capital plans, seeking to forecast problems in future years and address them before they become larger issues.

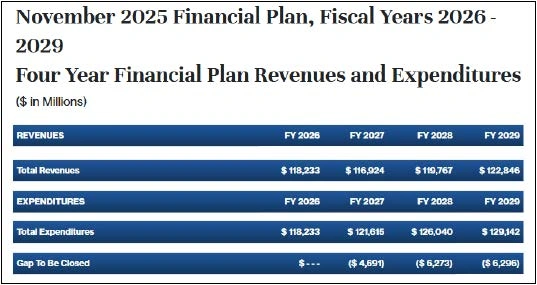

We've often found that when mainstream news runs stories on City fiscal deficits, the gap in question is simply a forecast several years in the future that assumes no corrective actions are taken today. But this is a feature, not a bug: identifying potential issues before they happen, and providing runway to fix them beforehand, is a sign of prudent management. That's exactly what we tend to see: NYC's perennially projects 'out-year' budget deficits that end up being proactively addressed and transformed into balanced books once those years actually arrive.

All of this isn't simply the result of voluntary cultural change - these procedures were forced into existence by New York State, which took a much tighter grip on the reins of the City's finances after the crisis. We mean this in a literal sense: immediately after the crisis the State established the NYS Financial Control Board, which had explicit power to reject City budgets and borrowing plans if they didn't meet strict multi-year maximum deficit limits. In fact, the Control Board still exists and oversees NYC's finances, albeit not in a 'hard control' fashion as the City has long since proved its ability to live and plan within those defined boundaries.

In addition to indirect guardrails, Albany has plenty of direct levers of control: any substantive proposed changes to the City's property, income, and sales tax regimes must be explicitly approved upstate via the regular State legislative and gubernatorial lawmaking process. NYS also exercises full operational and financial authority over the Metropolitan Transportation Authority (MTA), which is classified and managed as a state agency.

Importantly, we note that the State has a long history of fiscal restraint and responsible planning, as demonstrated by its own longstanding trend of balanced operations and sterling credit ratings.

If there's one point we want to emphasize, it's that NYC doesn’t have nearly as much unilateral power as you'd think. New York State retains effective veto power in almost every important financial matter. Moreover, it isn't just an empty threat - history is replete with examples of Albany refusing City requests for tax increases and other initiatives (remember the contentious City-State relationship during prior Mayor Bill de Blasio's tenure?). NYC can wish for the moon all it wants, but that doesn’t mean it’ll end up getting it.

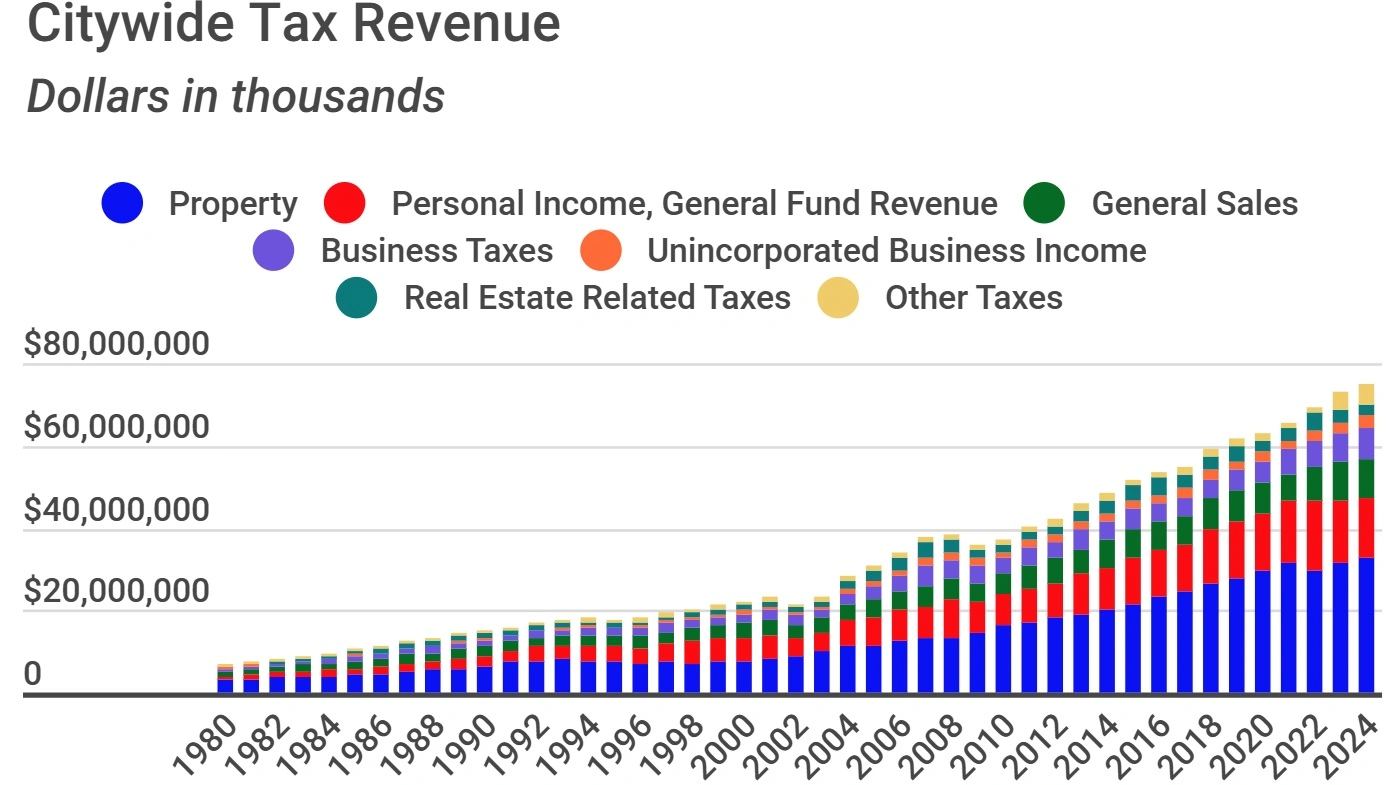

Now let's shift to the reality of what matters for NYC's financial health. Like most American local governments, the largest single source of funds is from property taxes. The City also levies a local income tax on residents and businesses, and ultimately receives approximately half of the sales tax that's collected by the State (NYS keeps the bulk of the remainder for itself). Other taxes plus state and federal grants also get added into the mix, but effectively these 3 tax streams are the workhorses of the budget.

Analyzing trends in the data that drive these critical revenues indicates that NYC's future financial prospects look to be as good as ever:

Property taxes are dependent on residential real estate values, which by every measure looks set to keep booming: rents are high and available apartments scarce, while selling prices continue to march higher every year. This decade's runup in home prices has certainly benefited the property tax levy, as tax bills are calculated as a percentage of assessed value (making this revenue stream positively affected by rising inflation).

Note that we highlight residential property data because commercial real estate taxes are a comparatively minor contributor to the City's total property tax haul.

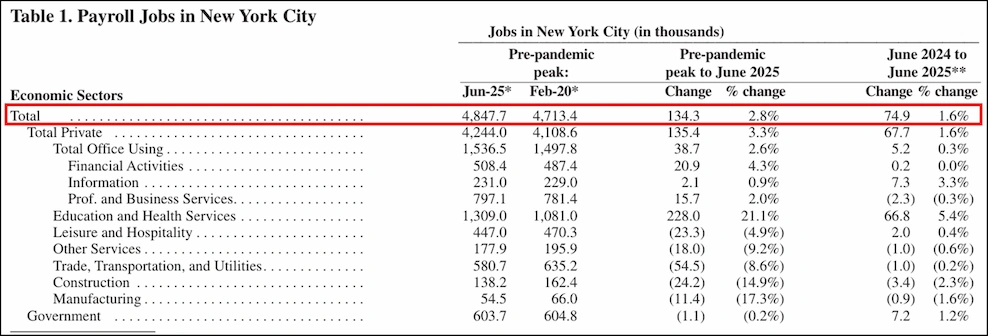

It's no wonder people are having a hard time finding vacant apartments in NYC, since the rising tide of workers need someplace to live. The city's population is once again growing, while total employment numbers have already exceeded their pre-pandemic peak. NYC's income tax collections are, intuitively, positively correlated with the health of its labor market.

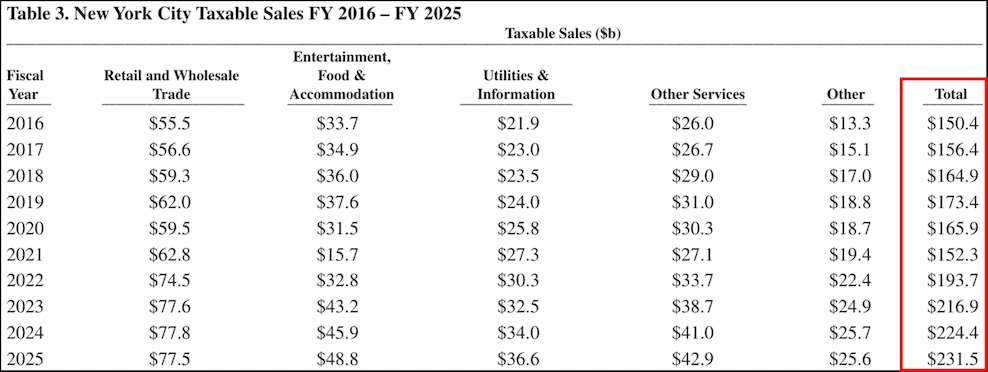

A healthy consumer is an employed one - after all, it's hard to keep buying things if the income isn't coming in! This healthy employment backdrop has led to strong and sustained spending activity, directly driving spiking sales tax collections (which, like property taxes, is a percentage-based revenue stream that automatically increases along with inflation).

Clearly NYC's essential sources of income seem to be in good shape, but of course that isn't the whole story. Municipal budgets are fundamentally like personal ones - it's always possible for expenses to outpace even the healthiest revenue hauls if balance isn’t prioritized.

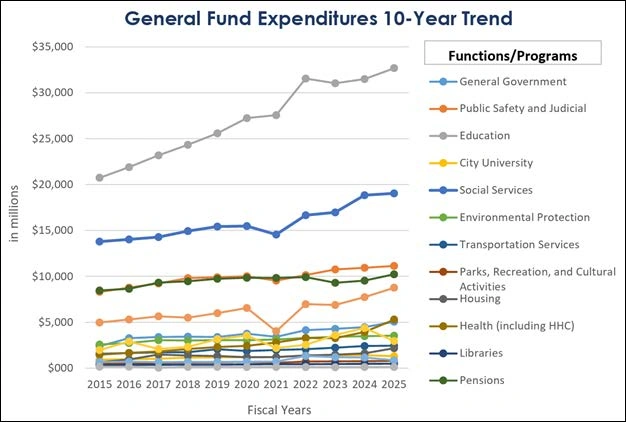

The City's General Fund expenses look fairly mundane: the lion's share of spending goes to quintessentially local responsibilities like funding schools (NYC schools, consistently the largest district in America, are a component department of its municipal government), public safety, and civil servants' salaries. The City does allocate a healthy portion of spending on social services, but within context of the overall budget it's just one of many line items.

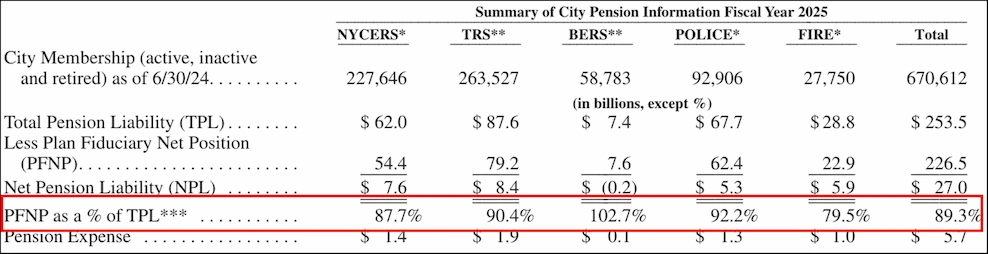

One positive note is that ongoing pension funding costs aren't the salient pressure point we often see elsewhere. Although you can't say the City's employee pension systems are a light burden to bear, NYC regularly sets aside enough money to keep them well-funded.

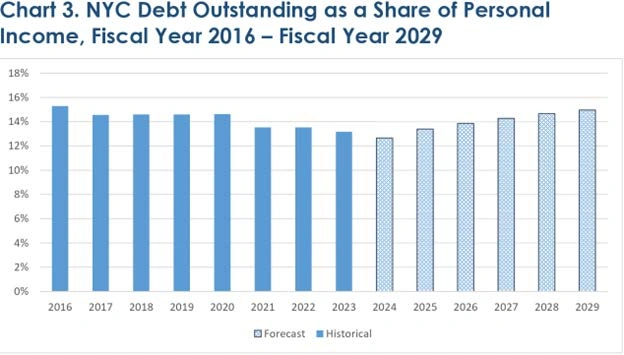

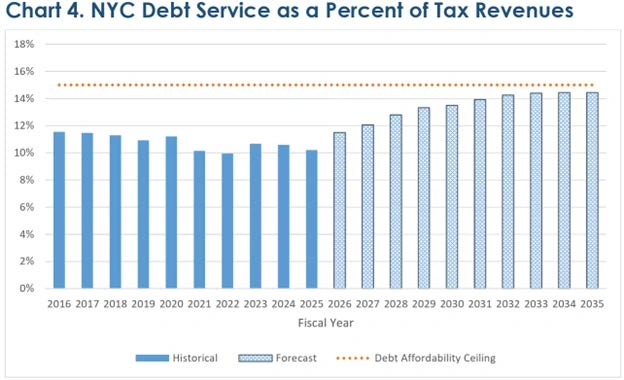

Relatedly, although NYC is without a doubt heavily indebted, those costs are quite reasonable. When measured as a percentage of residents’ income, the City's debt load has actually declined over time (and is forecast to stay broadly consistent with prior history). Meanwhile the cost of servicing that debt remains below its stated target of no more than 15% of own-source tax revenues.

The most important takeaway is that spending aligns with income – whether you agree or disagree politically with whoever's in the mayor's seat at any given time, modern NYC has consistently demonstrated the ability and willingness to live within its (considerable) means.

How does all this fit into the outlook for NYC muni bonds?

To bring everything full circle, another key objective of the reforms following the City's '70s financial crisis was to shore up NYC's ability to consistently access the municipal bond market. In addition to substantively improving the City's underlying financial situation, security features that enhanced bondholder protections were added to several of NYC’s major borrowing credits (as well as the temporary entity established to refinance some of the City's existing debt, the Municipal Assistance Corporation - older readers may remember the famous MAC). This was considered a necessity to reestablish investor confidence, which was crucial to restoring the constant flow of capital the City needs to fund its always-large infrastructure investments.

That legacy of enhanced legal protections and bondholder-friendly covenants lives on in today's NYC debt stack. Although the City's financial management practices and budgetary balance are now in very good shape, its key funding credits still carry unusually strong bondholder-friendly security features. NYC accomplishes its substantial capital borrowing needs by spreading the burden across several legally separate credits which are conservatively managed to maintain very high ratings from all the major credit rating agencies. We would also note that some key infrastructure assets serving the NYC metro area aren’t owned or operated by NYC government, and are thus not tied to its financial health (nor, for that matter, are they City government's responsibility to fund).

For added context, here are some very brief descriptions of several NY credits that we frequently purchase within client bond portfolios:

We've authored this white paper in response to client questions about how NYC's new Mayor Zohran Mamdani's aggressive social spending agenda could affect City finances and the credit outlook for its related municipal bonds. At this point our thinking is simple: although the situation bears monitoring, there's no reason to change our fundamental outlook or dial back existing exposures to NYC munis.

We hope this overview has provided readers with enough context to see for themselves why much of the negative hype circulating in mainstream news is overblown:

That being said, don't be surprised if headline risk ticks higher going forward. Mayor Mamdani clearly has a strong bias towards bold policy changes that, if enacted, would certainly require a fresh assessment of their fiscal implications.

But we would caution readers to remember that politics is the art of talking while governing is the art of doing. Executives get a lot of media attention (especially when they first rise to power), but securing results is a whole different ball game. NYC Mayors aren't dictators – not only do they have to secure State approval on anything that moves the needle, but they must also coexist with an often-combative City Council, which always has its own distinct interests and the power to advance them.

Naturally, we are actively monitoring the progress of Mayor Mamdani's initiatives and will continue to assess any and all impacts on portfolio positions.