With the Middle East at war and global supply chains ensnared by the conflict, market participants have been busy pricing in new risks and shifting outlooks. Now that the first quarter of 2026 is in the books, how should corporate cash investors position their portfolios in this rapidly shifting landscape? Read on for our current thoughts.

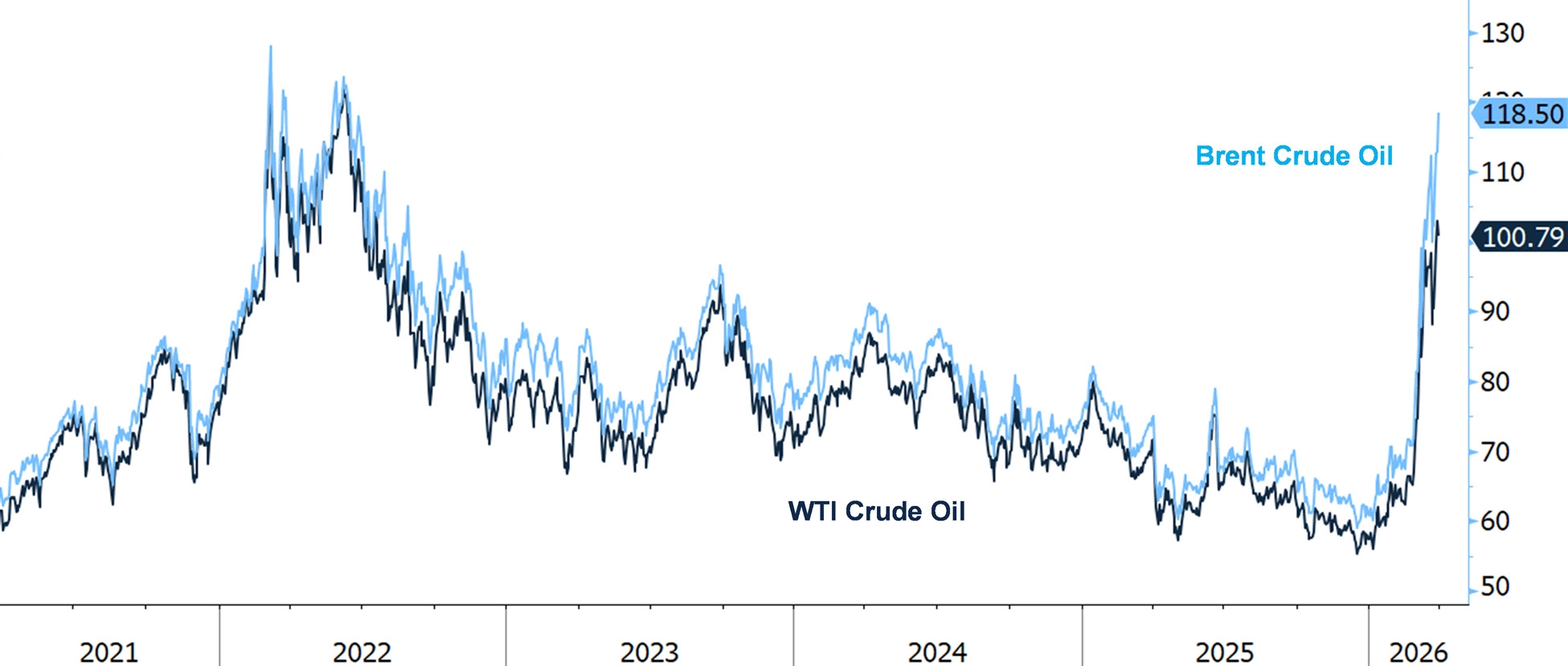

Thus far the primary economic impact from the Iran conflict flows from the disruptions to key commodity supply chains. The threat of Iranian attacks on ships transiting the strategically vital Strait of Hormuz has curtailed a significant proportion of the world’s supply of petrochemicals, causing oil and gas prices to surge to levels last seen following 2022’s Russian invasion of Ukraine. The secondorder spillover effects of this spike are also massive, with natural gas a critical feedstock in the production of fertilizer and plastics. Moreover, a large percentage of the world’s production capacity in aluminum and helium (the latter an essential input in the production of microchips) is in the Middle East and also effectively stuck within the Persian Gulf. In short, it’s a bona fide logistical mess.

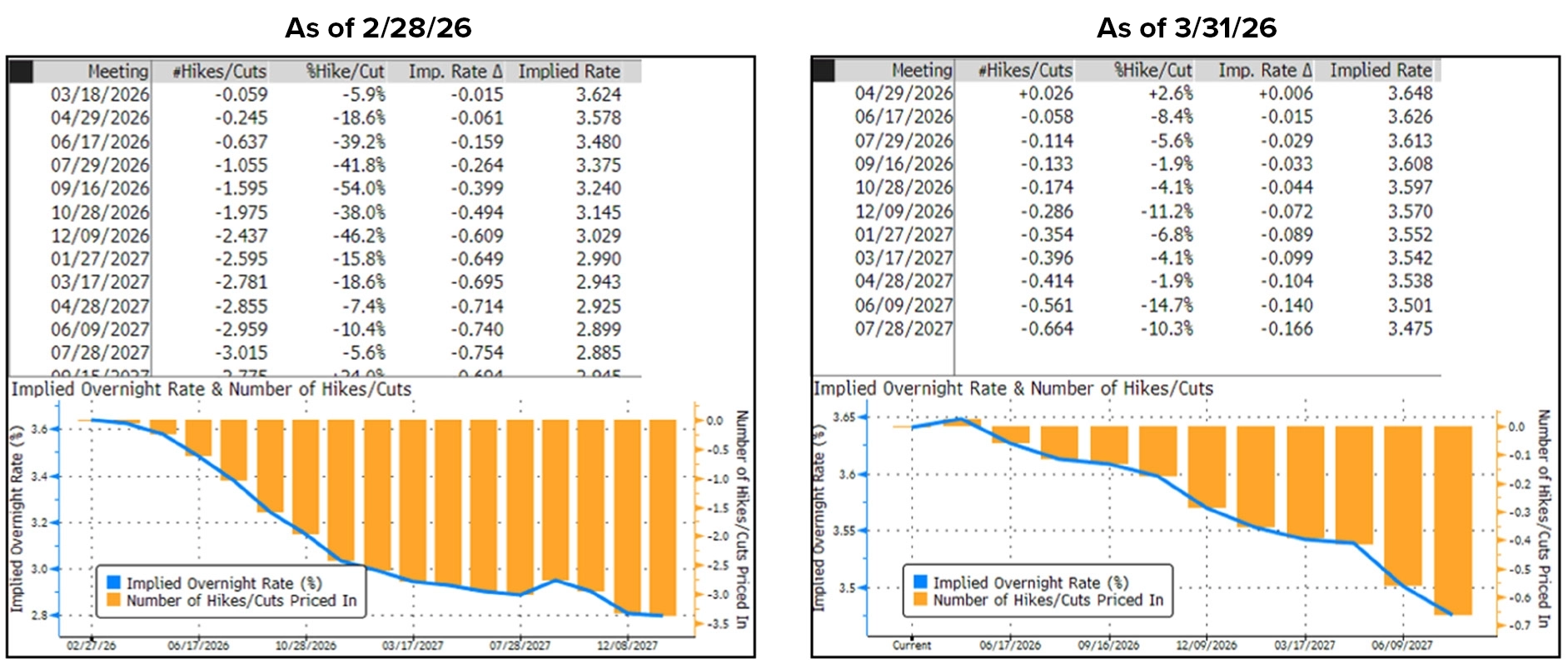

The natural aftermath of all this is rationing and higher prices. While the US fortunately has the domestic petrochemical production capacity to prevent the former (unlike Asia and possibly Europe), it isn’t immune from the latter. Combined with an inevitable uptick in the federal government’s deficit - American aircraft carriers and Tomahawk missiles don’t fund themselves - fixed income markets foresee renewed inflationary pressures forming and have reacted by quickly eliminating the prospect of near-term Fed rate cuts.

Just one month ago markets were projecting at least 2 rate cuts before the end of 2026, reflecting a solid pre-war real economic environment. Fast forward to today, and fears of higher inflation (and possibly even stagflation) have meaningfully downshifted bond investors’ expectations to no longer anticipate any Fed action until the summer of 2027.

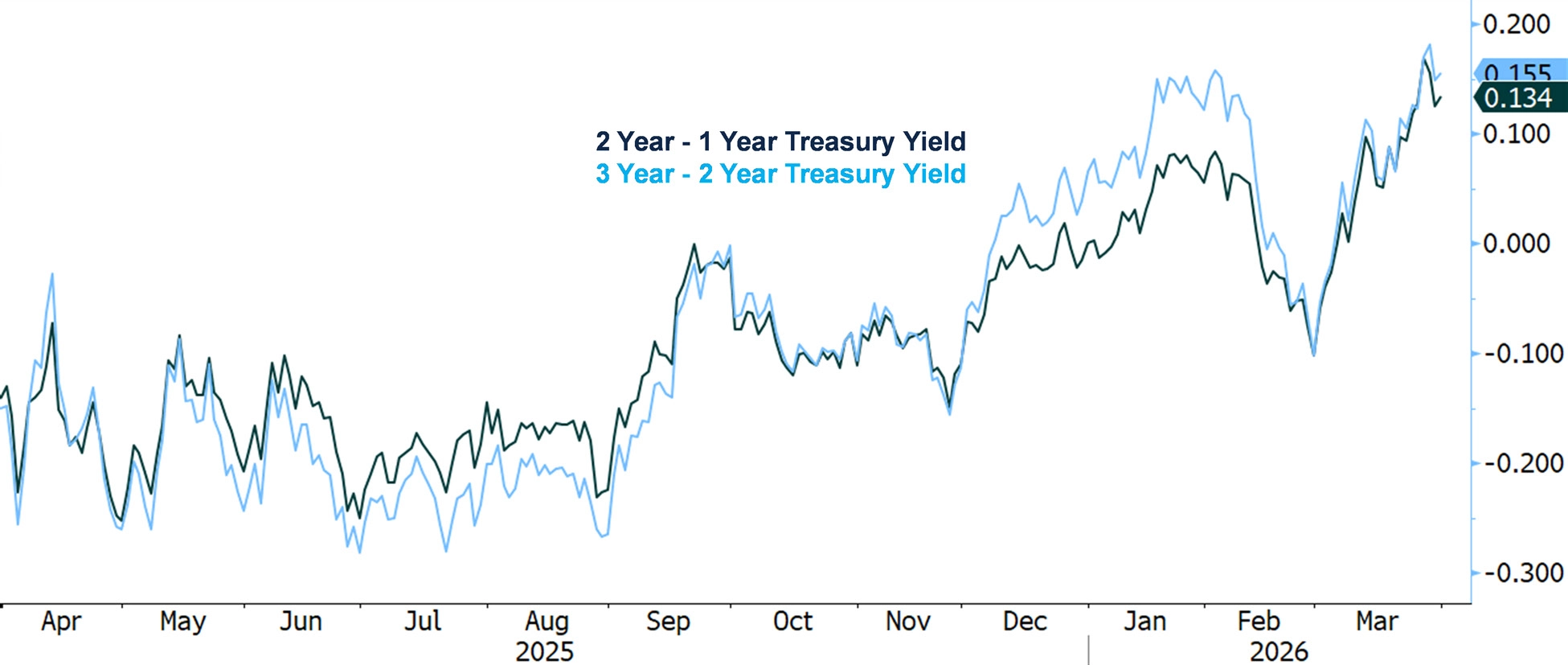

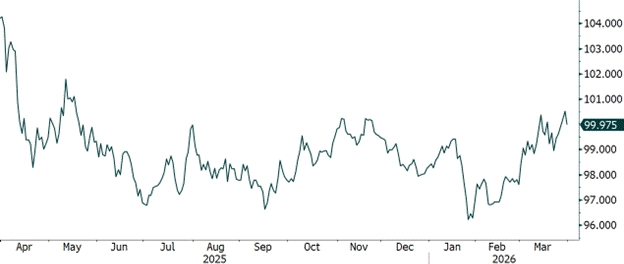

The net result has seen front-end rates rise significantly over the past month in what is known as a 'bear steepener' pattern. Absolute levels have increased meaningfully, albeit the scale of the move is much more subdued when compared to where yields were trading just 6-12 months ago.

Meanwhile the yield differential between longer versus shorter maturities has widened. We’ve transitioned from an inverted/essentially flat yield curve to one that is positively sloped, where positive yield pickups vs. government money market funds (currently yielding 3.55-3.60%) are available even on very short Treasury bills.

The headlines driving today’s developments revolve around analyzing the first-order effects of the commodity supply shock. But markets don’t stand still: to understand what will drive tomorrow’s rate moves – which is what matters for positioning bond portfolios – we must focus on the demand side of the equation. Ultimately it will all come down to how well the real economy absorbs the price spikes.

If a resolution comes swiftly, with supplies quickly coming back online and prices largely retracing their wartime spike, then the fallout is likely to be contained. In this scenario the past month would be just an interesting footnote in economic history, and the market narrative would refocus on the benign backdrop that was in place before the shooting began: subdued inflation, solid corporate fundamentals, and continued earnings and wage growth. The Fed would probably look through a few months' worth of higher commodity prices as a transitory shock, and investors would likely go back to assuming a bias towards gradually reducing rates going forward.

But the longer this conflict drags on, the harder the squeeze on underlying demand. Higher oil and gas prices will inevitably leech into the cost of goods and services over time, setting a higher baseline for inflation expectations that leads to belt tightening by producers and consumers alike. This demand destruction, if allowed to continue unchecked, would eventually cause economic activity to slow, undoubtedly catching the Fed’s attention. The Fed has an explicit dual mandate to balance price stability with full employment, and in this scenario would be caught between a rock (tighten monetary policy to combat inflation) and a hard place (cut rates to counter flagging growth and likely rising unemployment). Given the political reality of the situation – particularly so given that the Fed’s new management has been hand-picked by a presidential administration that clearly wants lower rates – the Fed would almost certainly lean towards easing conditions to bolster labor markets.

Here’s the important takeaway: in either of these scenarios, note that the Fed is not raising rates. Whether this renewed inflationary impulse proves temporary or more durable, it’s very difficult to imagine a Fed helmed by a newly installed Chairman Kevin Warsh would react by hiking rates. This has crucial implications for our rates forecast, pointing to today’s levels as an opportunity worth capturing before they fade.

As an aside, our focus is on domestic dynamics for game-planning the path of domestic yields. The situation facing the US economy and fixed income markets is notably different from what other major economies are experiencing.

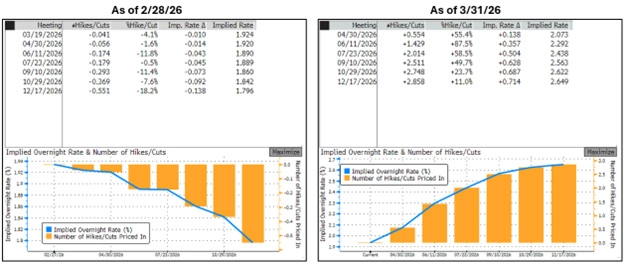

For example, the Eurozone is more directly exposed to the brunt of the commodity supply shock – Europe is directly dependent on Middle Eastern petrochemical supplies for its energy needs (unlike the more self-sufficient US). Moreover, the European Central Bank is a single mandate institution with a primary objective to keep inflation in check. The ECB has far less leeway to look through inflation spikes and weigh the countervailing effects of longer-run demand destruction, which essentially forces them to hike Eurozone rates into the teeth of looming stagflation if the situation persists. It’s a far bleaker and more constrained set of options than those available in the Federal Reserve’s toolbox, and developments in the Eurozone’s yield curves reflect this reality. Last month markets penciled in 50/50 odds of an ECB rate cut by December - now they assume nearly 3 hikes!

Contrast that to the US: Fed Funds Rate expectations are pricing off totally different decision paths, with ample evidence that a safe haven flight-to-quality bid has also factored into the market’s calculus. We’ve already seen the US dollar strengthen since the war began, an unsurprising development with plenty of historical precedent. In short, the US markets play by a different set of rules.

First things first - our base case assumes the conflict resolves within the next 90 days. Any longer than that will likely trigger a larger global problem which all participants have an interest in avoiding. A resolution would see a resumption in the flow of key commodities, allowing price spikes to gradually retrace over the coming months. Although damage will have been done, the inflationary shock will prove temporary, and the primary driver of this past month’s rates spike should begin to fade. That should, in turn, return us to the stable fundamental landscape that was in place before the shooting started.

Recall how benign pre-war conditions were: solid economic growth was backed up by supportive fiscal policy, robust corporate earnings and balanced labor markets. In addition to these positive cyclical indicators, the secular trend of tech-driven productivity gains is primed to boost the real economy’s potential growth rate for years to come.

This productivity growth story is also proving to be a powerful force in keeping longer-run inflation expectations in check. Even today, in the midst of a commodity price shock, longer-run inflation breakevens continue to decline. Bet against this trend at your own risk.

Assuming hostilities quickly cease, the bottom line is simple – this is probably a temporary rate spike that is likely to fade sooner rather than later. Forward-thinking corporate cash investors should regard it as an unexpected opportunity to extend maturities at elevated rates, locking in attractive portfolio book yields ahead of a return to a lower-rate environment in the coming quarters.