After a turbulent 2025, how are the economy and markets set up to enter 2026? Read on for our latest thoughts for corporate cash investors.

The market narrative entered 2025 with widespread concern that some of the new Trump Administration's policies would create inflation and unintended negative economic consequences. Most forecasters felt that strong protectionist instincts would impede global trade and cause a wide range of outcomes, from outright recession to stagflation.

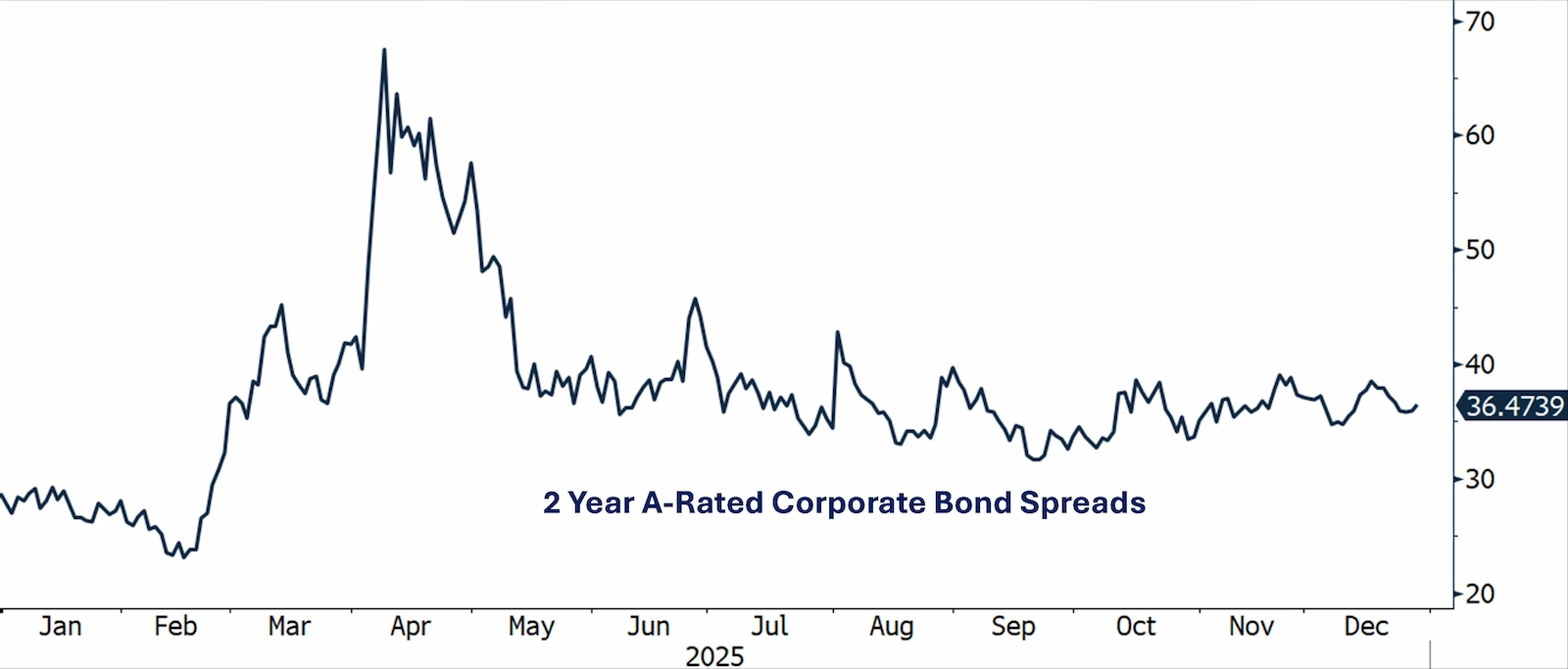

April's "Liberation Day" turned out to be a momentous pivot point in this regard, as a sweeping new tariff regime was unveiled to the surprise of investors who clearly hadn't expected either its scope or magnitude. As both rate and equity markets gyrated while digesting the unwelcome surprise, it became increasingly clear that it would take time to assess the true impact of these major changes to the economy and Corporate America's fortunes.

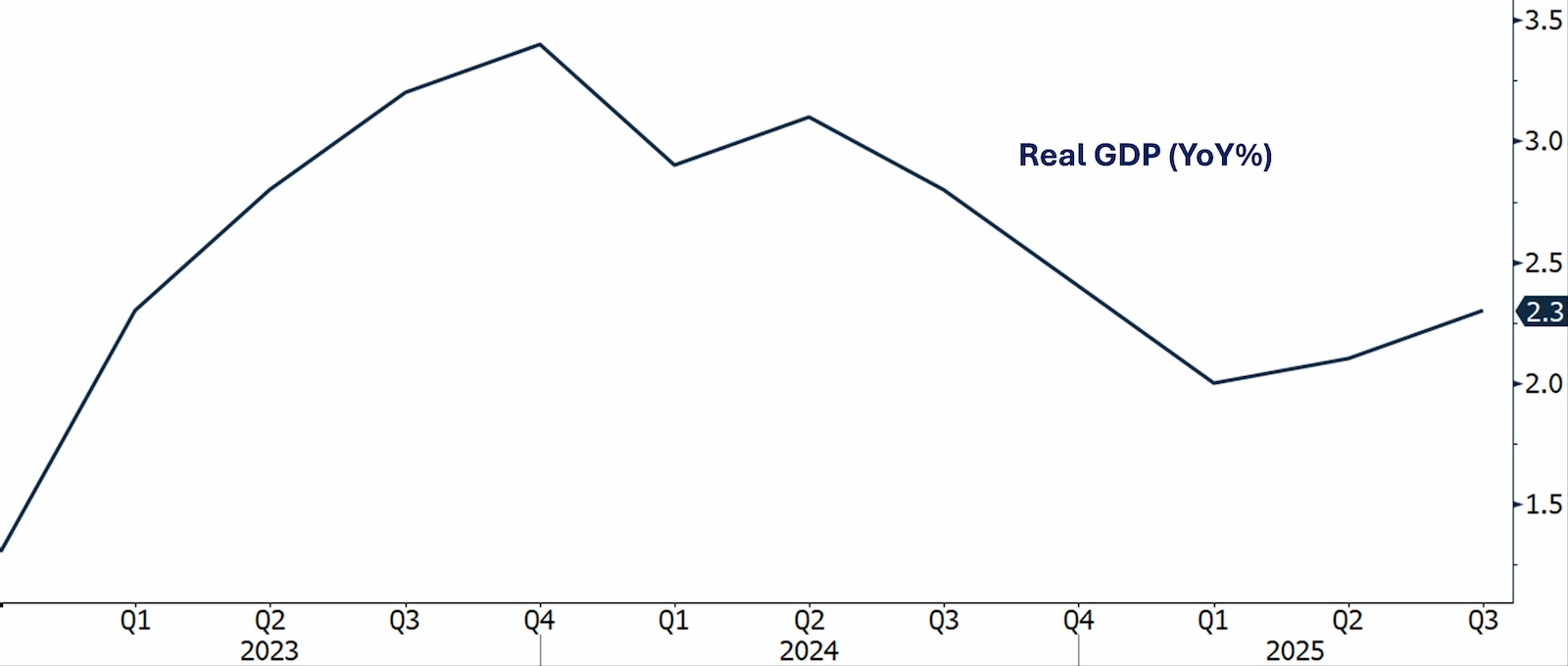

As we wrap up this tumultuous year, we can now see that the initial effects haven't been nearly as damaging as feared. From a top-down perspective, economic growth has remained solid, continuing the multi-year positive streak.

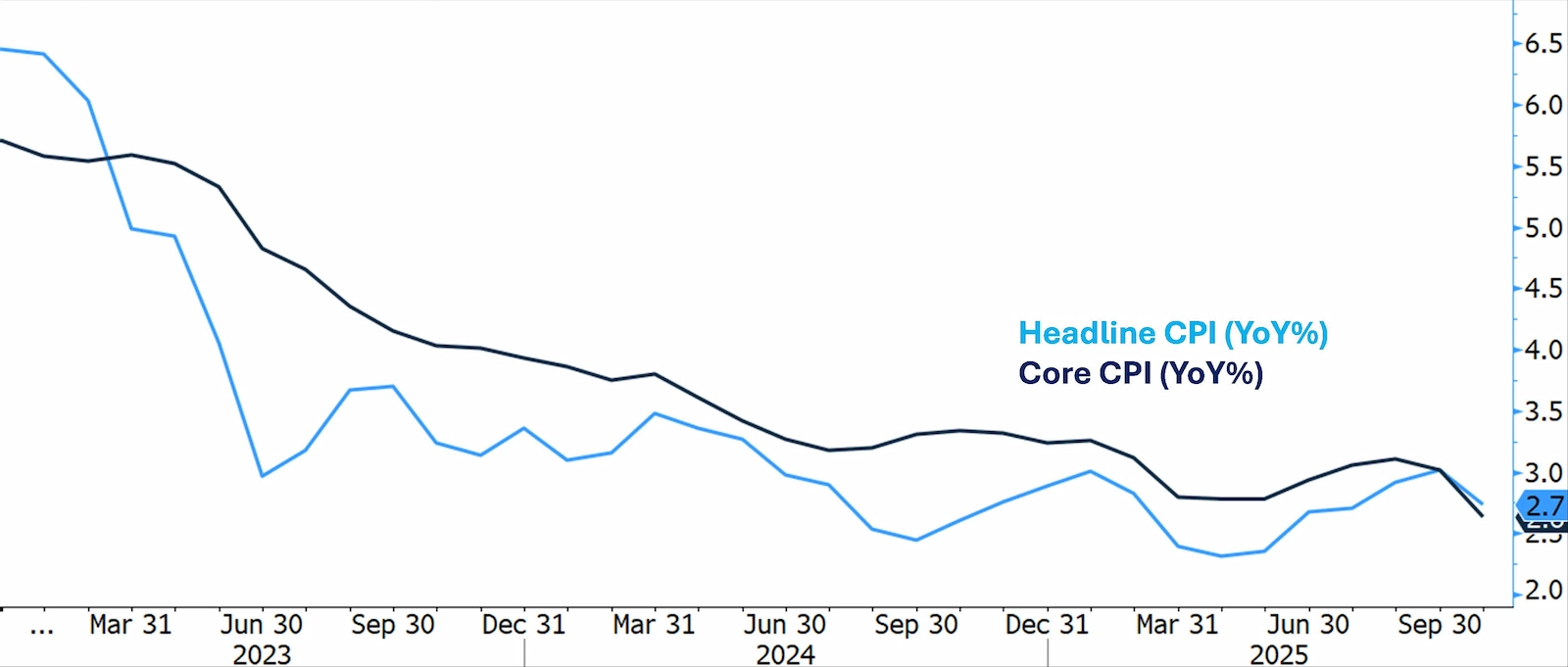

Perhaps the most widely anticipated downstream result of the new tariffs was that they would spur an increase in inflation. But in reality, both headline and core CPI measures have hardly budged. Although for now somewhat stalled above the key 2% historical target, we're still well below the historic post-pandemic highs of 2020-2023.

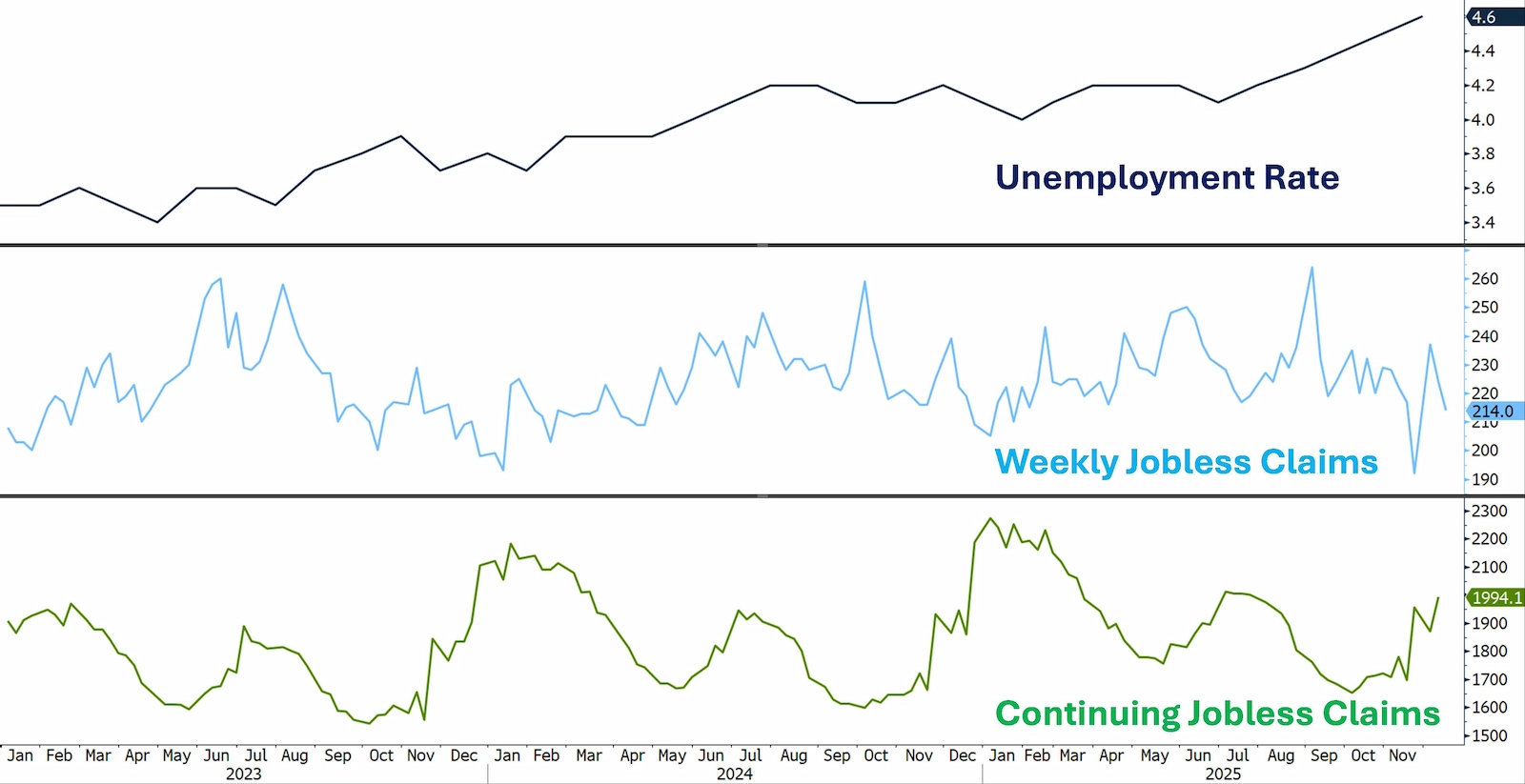

Tariffs weren't the only Trump policy causing investor angst - an emphasis on renewed enforcement of immigration laws, including a large uptick in the pace of deportations of undocumented immigrants, lead to fears of worker shortages and resulting higher wages for the remaining labor force. Not only did inflation measures overcome this headwind, but employment metrics also remained healthy throughout 2025, as the unemployment rate, jobless claims, and continuing claims reflect little cause for major concern. However, underlying the official numbers we can see some components of the overall unemployment rate ticking slightly higher, including the highest unemployment rate for recent college grads since 2015.

This fundamentally firm backdrop ultimately provided the Federal Reserve with sufficient comfort to continue easing monetary policy, as they cut the benchmark Fed Funds Rate by 75 basis points in the latter months of the year. Front-end rates reflected the moves in near lockstep, with 6 month and 1 year Treasury bill rates tumbling by 67 and 68 bps, respectively.

The yield curve roughly maintained its shape as intermediate-term rates declined by similar amounts, with 2 year and 5 year Treasury yields decreasing by 77 and 66 bps, respectively.

The benign conditions also proved a boon to Corporate America, as management teams successfully navigated the uncertain and tricky environment to deliver strong earnings growth.

Coupled with strong investor demand for risk assets, corporate bond credit spreads settled into a low and stable holding pattern after the initial post-Liberation Day spike.

As clients and past readers know, we rejected calls for the end of American exceptionalism, material flight from US dollar assets, rampant inflation, and the other assorted litanies of fear mongering from earlier in the year. We've instead extended maturities for our corporate cash clients throughout 2025, with the view that any negative economic impacts from the 'tariff-turmoil' were ultimately self-inflicted wounds that could, in turn, also be self-corrected if necessary. Further, we never agreed with the then-popular view that end consumers would bear the full burden of the tariff levies (and thus be forced to moderate their spending).

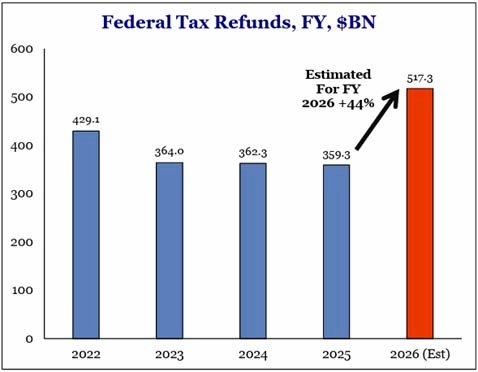

Looking forward, many of the undeniably positive policy changes – from new tax incentives to deregulatory initiatives – are primed to have much more of an impact in 2026 than they did for this past year. 2025's One Big Beautiful Bill Act (OBBBA) was a major piece of tax legislation that not only extended existing tax rates but added material incremental stimulus for both consumers and businesses alike. For our purposes, it's important to note that much of this stimulus hasn't even come online as of this writing. Specifically, the single largest item – a package of reduced tax rates and expanded deductions for individuals - was designed to come into play in 2026, as income tax withholdings weren't adjusted to reflect the new reality.

The upshot is that the American consumer, the economy's fundamental underlying growth engine, is poised to reap a cashflow bonanza within the next few months as plumper-than-usual tax refund checks begin hitting bank accounts.

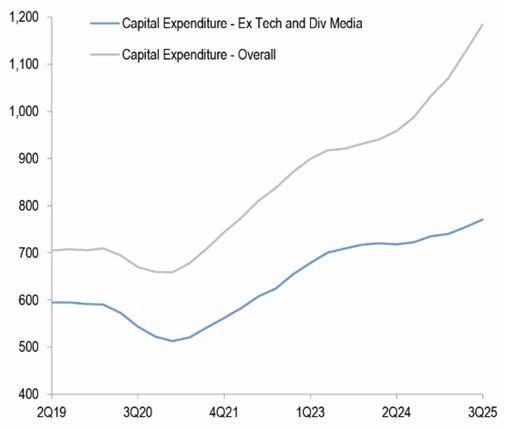

Businesses have their own set of concessions to enjoy, particularly 100% bonus depreciation and front-loaded deductions for research and development expenses (in which the full cost of R&D can be deducted in the year during which funds were spent). Companies are already reacting to these favorable new incentives by ramping up capital expenditures, traditionally a harbinger of increased productivity in future quarters. Moreover, in addition to these 'hard' incentives, the 'soft' inducements have also gotten more enticing as deregulation and measures to ease permitting requirements and timelines are also making it easier to pull the trigger on new projects.

Not to be forgotten are the continuing fundamental tailwinds from the boom in Artificial Intelligence, which shows little signs of slowing down. Corporate America is all-in on the AI revolution, as capex devoted to AI-related projects has become the dominant driver of most long-term investment activity. Note that AI-related spending has wide-reaching effects on many related sectors - e.g. the construction and materials industries supporting data-center buildouts and electric generation ramp-ups are prime beneficiaries. Far from reaching a crescendo, it's much more likely we're in the early stages of this trend, with broad downstream effects that will only become more apparent with time.

We expect continued economic growth in 2026 due to still-healthy labor market data, declining inflation measures, mounting federal fiscal stimulus, and ongoing benefits from the massive flywheel that is the AI infrastructure surge.

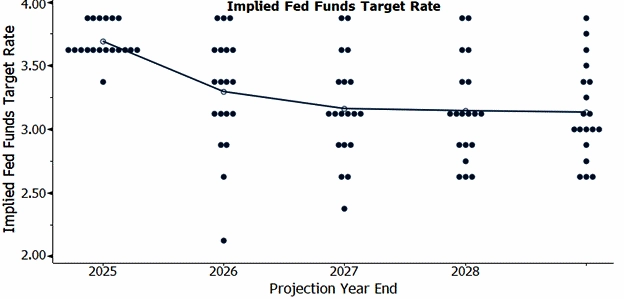

But this solid backdrop is only one factor that goes into determining how markets trade. For corporate cash investors, the outlook for Fed policy is crucial, as expectations for the future course of the Fed Funds Rate are the dominant driver of front-end yields. Despite the healthy economic data, Fed officials are signaling even more rate cuts are on the docket for 2026. This is generally the opposite of what traditional economic orthodoxy would recommend, as cutting rates is typically reserved for times when monetary easing seems necessary to revive a flagging real economy.

Why this deviation from the usual playbook? It's because the Fed's dual mandate - to stabilize price pressures along with maintaining the health of the labor market - must also be balanced against political considerations. As we wrote a few months ago:

"Normally a healthy economic setting implies steady to rising front-end rates, but that's not the case this time. In fact, the Federal Reserve has already started cutting the Fed Funds rate while signaling further easing should be expected…Why the easing despite a reasonably healthy economy? Remember that personnel create policies. Fed Chair Powell's term ends early next year, and although the Trump Administration is still interviewing candidates to replace him, it's abundantly clear the President prefers those who appear committed to further meaningful rate cuts. There's no need to overthink this observation…It stands to reason that future Fed appointments, including for the Chair's position, will likely hold similar philosophies." (Corporate Cash Alert: Extend is Your Friend, 10/14/25)

Personnel equals policy, and over time political influence over the Fed's decisions can become decisive as those sympathetic with the President's viewpoints assume a greater share of decision-making power. In addition to appointments to the Board of Governors, the all-important choice for a new Fed Chair is imminent, and the President has made clear he considers having a clear bias towards lowering rates is a non-negotiable requirement for the position.

The core message sounds loud and clear to us – expect lower short-term rates going forward. While concerns about inflation and the consequences of weakened Fed independence are valid, it's highly likely these would primarily be reflected in a repricing of long-term rates and equity markets rather than in the maturity ranges and credit spreads that concern corporate cash investors. Moreover, although absolute yields available in today's environment are undoubtedly lower than we've seen over the past couple of years, they remain at very reasonable levels.

Reinvestment risk – the possibility that rates will be even lower when currently-held positions naturally mature and must be rolled over into new holdings at then-current market levels – strikes us as the more salient concern at this juncture. As always, the tried-and-true method for mitigating reinvestment risk is to extend maturities, and lock in current yields for as long as Investment Policy constraints permit. We've been (loudly!) ringing the bell to extend maturities in corporate cash portfolios for the past couple of years and today is not the day we change our tune.